Quick Answer

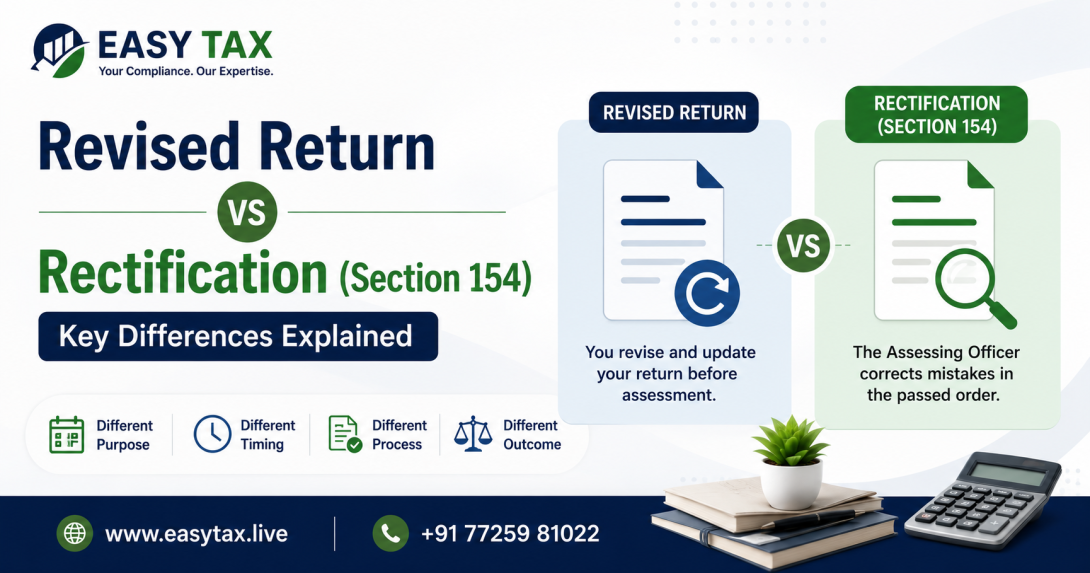

A Revised Return under Section 139(5) is used when you discover an error or omission in an Income Tax Return that you have already filed. In contrast, Rectification under Section 154 is meant to correct only a mistake apparent from the record, such as calculation errors, incorrect tax credits, or clerical mistakes, after the Income Tax Department has processed your return. Choosing the correct option helps avoid delays, notices, and refund issues.

Many taxpayers discover mistakes after filing their Income Tax Return (ITR). Sometimes the error is as simple as entering the wrong bank account number, while in other cases important income, deductions, or tax credits may have been omitted. When this happens, taxpayers often wonder whether they should file a revised return or submit a rectification request under Section 154. Although both options are used to correct mistakes, they serve different purposes and follow different legal provisions.

Understanding the difference between a revised return vs rectification is important because selecting the wrong option may delay your refund, trigger additional verification, or even result in an unnecessary notice from the Income Tax Department. The right approach depends on the type of mistake, the stage of processing, and the applicable provisions of the Income Tax Act.

In this guide, you'll learn what a revised return is, how Section 154 rectification works, when each option should be used, their key differences, and how to decide which is appropriate for your situation.

What Is a Revised Return?

A Revised Return is a fresh Income Tax Return filed under Section 139(5) to correct errors or omissions in an originally filed return. It replaces the earlier return and enables taxpayers to report the correct income, deductions, exemptions, tax credits, or other information before the applicable deadline.

A revised return is commonly used when taxpayers discover mistakes such as:

- Incorrect reporting of salary or business income.

- Missing bank interest or capital gains.

- Failure to claim eligible deductions.

- Incorrect personal or bank account details.

- Omission of TDS or advance tax information.

- Errors in reporting house property or other income.

If you need to revise your return, our detailed guide on Revised ITR Filing explains the complete process.

What Is Rectification Under Section 154?

Rectification under Section 154 allows taxpayers to request correction of a mistake apparent from the record after the Income Tax Department has processed the return. Unlike a revised return, rectification is not meant for changing income figures or adding new deductions that were omitted while filing the return.

Section 154 is generally applicable for obvious mistakes such as:

- Mathematical or calculation errors.

- Incorrect tax credit appearing in the processed return.

- TDS mismatch due to processing issues.

- Clerical or data entry mistakes.

- Errors in tax computation by the department.

If the mistake requires changing your declared income or adding new information that was omitted, filing a revised return is generally the more appropriate option rather than submitting a rectification request.

Revised Return vs Rectification: Key Differences

Although both procedures are used to correct mistakes, they differ significantly in purpose, scope, and legal provisions. Understanding these differences helps taxpayers choose the correct remedy.

| Particulars | Revised Return | Rectification (Section 154) |

|---|---|---|

| Applicable Provision | Section 139(5) | Section 154 |

| Purpose | Correct omissions or mistakes in the filed ITR | Correct mistakes apparent from the record |

| Can Income Be Changed? | Yes | Generally No |

| Filed By | Taxpayer | Taxpayer or Income Tax Department |

| Suitable For | Major corrections and omitted information | Apparent errors after processing |

When Should You File a Revised Return?

A revised return should be filed whenever the original Income Tax Return contains incorrect information or misses important details that affect your taxable income or tax computation. Filing a revised return ensures that the Income Tax Department receives the correct financial information before the applicable deadline.

You should consider filing a revised return if you:

- Forgot to report an income source.

- Claimed an incorrect deduction or exemption.

- Entered incorrect bank account information.

- Reported the wrong TDS or advance tax details.

- Made mistakes while selecting your ITR form.

- Need to update information before the permitted deadline.

Before filing a revised return, make sure your original Income Tax Return (ITR) has been filed correctly and verify whether you are still within the applicable time limit. If you're unsure about the correct return form, refer to our guide on Which ITR to File.

Made a mistake while filing your Income Tax Return? EasyTax's experts can help you determine whether a revised return or a Section 154 rectification request is the right solution and ensure your return is corrected accurately.

Correct Your ITR with EasyTax

When Should You File a Rectification Request?

A rectification request under Section 154 should be filed only when there is a mistake apparent from the record. These are obvious errors that can be identified without further investigation or interpretation of tax laws. A rectification request is generally submitted after the Income Tax Department has processed your return and you notice an error in the processed order.

You should consider filing an ITR rectification request in situations such as:

- Tax credit or TDS has not been correctly considered.

- There is an error in tax computation.

- A clerical or calculation mistake exists in the processed return.

- The refund amount has been incorrectly calculated due to a processing error.

- An apparent mistake exists in the Income Tax Department's order.

If the correction requires adding omitted income, claiming a new deduction, or changing financial details, a revised return—not rectification—is generally the appropriate option.

Section 154 Time Limit

A common question taxpayers ask is about the Section 154 time limit. A rectification request can only be made within the period prescribed under the Income Tax Act. Since tax provisions may change over time, taxpayers should always verify the latest applicable deadlines before submitting a request.

Similarly, revised returns under Section 139(5) must also be filed within the prescribed time limit. Missing these deadlines may require exploring other available options, such as filing an updated return where applicable.

If you're unable to revise your return within the permitted period, you may wish to learn more about ITR-U Filing and understand when an updated return can be filed.

Practical Examples

The following examples make it easier to understand the difference between a revised return and rectification.

| Situation | Recommended Action |

|---|---|

| Forgot to report bank interest income. | File a Revised Return. |

| Entered the wrong bank account details. | File a Revised Return. |

| TDS credit not considered after processing. | Submit a Rectification Request. |

| Tax calculation error in the processed order. | Submit a Rectification Request. |

| Forgot to claim an eligible deduction. | Generally, file a Revised Return if within the prescribed time limit. |

Received an Income Tax notice or unsure whether to revise your return or submit a rectification request? EasyTax's experts can review your case and recommend the correct course of action.

Resolve Your ITR Issues with EasyTax

Common Mistakes to Avoid

Choosing the wrong correction method can delay refunds or lead to unnecessary correspondence with the Income Tax Department. Keep these points in mind:

- Don't use Section 154 to report omitted income.

- Don't file a revised return for simple processing errors that qualify for rectification.

- Always verify Form 26AS, AIS, and TIS before filing or revising your return.

- Complete your ITR e-Verification promptly after filing.

- Track your ITR Refund Status after corrections are processed.

- Respond promptly if you receive any Income Tax Notice.

Frequently Asked Questions (FAQs)

What is the difference between a revised return and rectification?

A revised return corrects mistakes or omissions in the original Income Tax Return, while rectification under Section 154 is used to correct mistakes apparent from the record after the return has been processed.

Can I file both a revised return and a rectification request?

Yes, but they serve different purposes. The appropriate option depends on the nature of the error and the stage of processing of your return.

Can I change my income through a Section 154 rectification request?

Generally, no. Section 154 is intended for correcting apparent mistakes and not for reporting omitted income or making substantial changes to the return.

What if I missed the deadline for filing a revised return?

Depending on your circumstances, you may explore options such as filing an updated return where permitted under the Income Tax Act.

How do I know which correction option is right for me?

Review the nature of the mistake carefully. If you're uncertain, consult a tax professional before submitting either a revised return or a rectification request.

Conclusion

Understanding the difference between a revised return vs rectification is essential for correcting Income Tax Return errors efficiently. A revised return under Section 139(5) is appropriate when you need to correct or update information in your original return, whereas rectification under Section 154 is intended for correcting obvious mistakes that appear in the records after processing.

Before choosing either option, review your return carefully, verify your tax documents, and understand the applicable time limits. Taking the correct approach can help you avoid delays, notices, and refund issues while ensuring compliance with the Income Tax Act.

If you need assistance with filing a revised return, submitting a rectification request, responding to an Income Tax notice, or resolving any ITR-related issue, visit EasyTax or contact our experts through the Contact Us page for personalized support.